You might have heard of payment orchestration - the idea of sitting one layer above your payment providers to control how transactions are routed, retried, and optimized. It's become a standard part of how serious payment operations are built today.

Fraud orchestration works on the same principle, but applied specifically to risk.

Instead of managing fraud through a single tool or a fixed set of rules, fraud orchestration brings all your fraud signals - custom rules, third-party fraud tools, device intelligence, behavioral data - into one coordinated layer. That layer evaluates every transaction in real time and decides what happens next: approve it, block it, route it for review, or step it up with additional verification.

What Fraud Orchestration Actually Is

Payment fraud detection has historically been fragmented. You'd have one tool checking card details, another flagging IPs, and maybe a manual review queue somewhere in the middle. Each of these works in isolation. In many setups these systems operate in silos, with limited coordination between them. Signals exist, but they're evaluated independently - which makes it harder to form a complete view of risk.

Fraud orchestration pulls everything into a single, coordinated layer. It evaluates each transaction against your risk rules, your risk lists, and signals from third-party fraud tools then makes a decision: approve, block, or flag for review.

”Optimizing payment costs saves money, but optimizing fraud decisions protects revenue. Payments and fraud decisions are deeply interconnected. A transaction optimized purely for cost or routing can still fail if fraud risk isn’t evaluated correctly. At the same time, overly strict fraud checks can block legitimate customers and reduce conversion.” - Ahmed Salem Elzeiny, Lead Solution Architect MoneyHash

The "orchestration" part means you control the logic. If a transaction triggers a risk rule but scores low on device fingerprinting, what happens next? With a fraud orchestration system, you define that. You're not waiting on a black box to decide. This is what separates a proper fraud management solution from a standalone fraud tool. One gives you coverage. The other gives you control.

How It Works in Practice

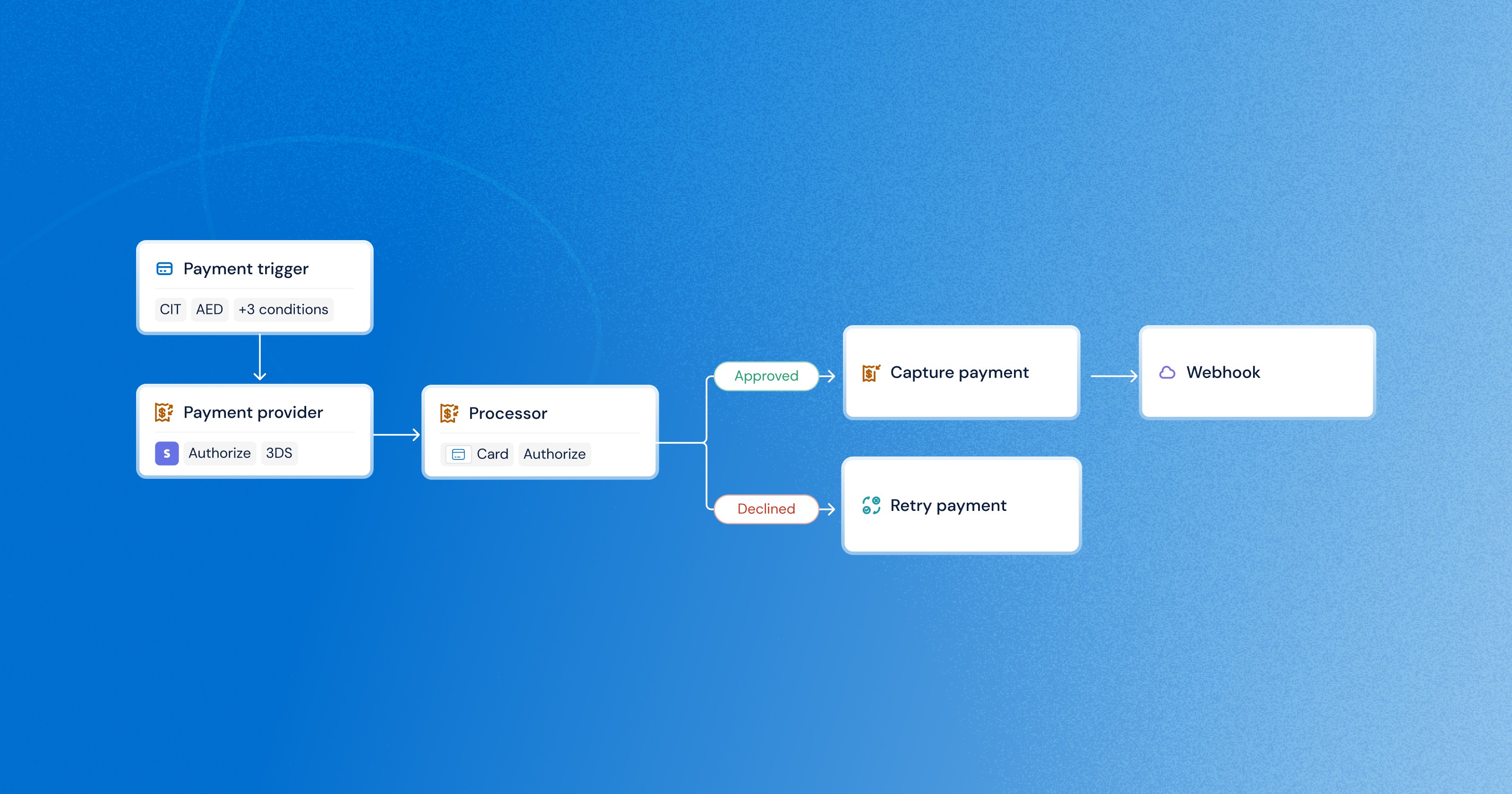

Here's a straightforward example. A customer initiates a payment. Before that transaction ever reaches a payment provider, your fraud orchestration layer runs through a sequence you've configured:

Check risk lists such as email, IP address, device ID, or BIN.

Evaluate transaction signals - amount, location, device fingerprint, and historical behavior.

If risk signals appear, send the transaction to a third-party fraud tool for deeper analysis.

Based on the combined signals, decide whether to approve the transaction, block it, require 3DS authentication, or send it to manual review.

And the whole process happens in real time - typically within a few milliseconds - so customers experience no additional friction during checkout.

That's online payment fraud prevention done right - not by adding more walls, but by adding more intelligence.

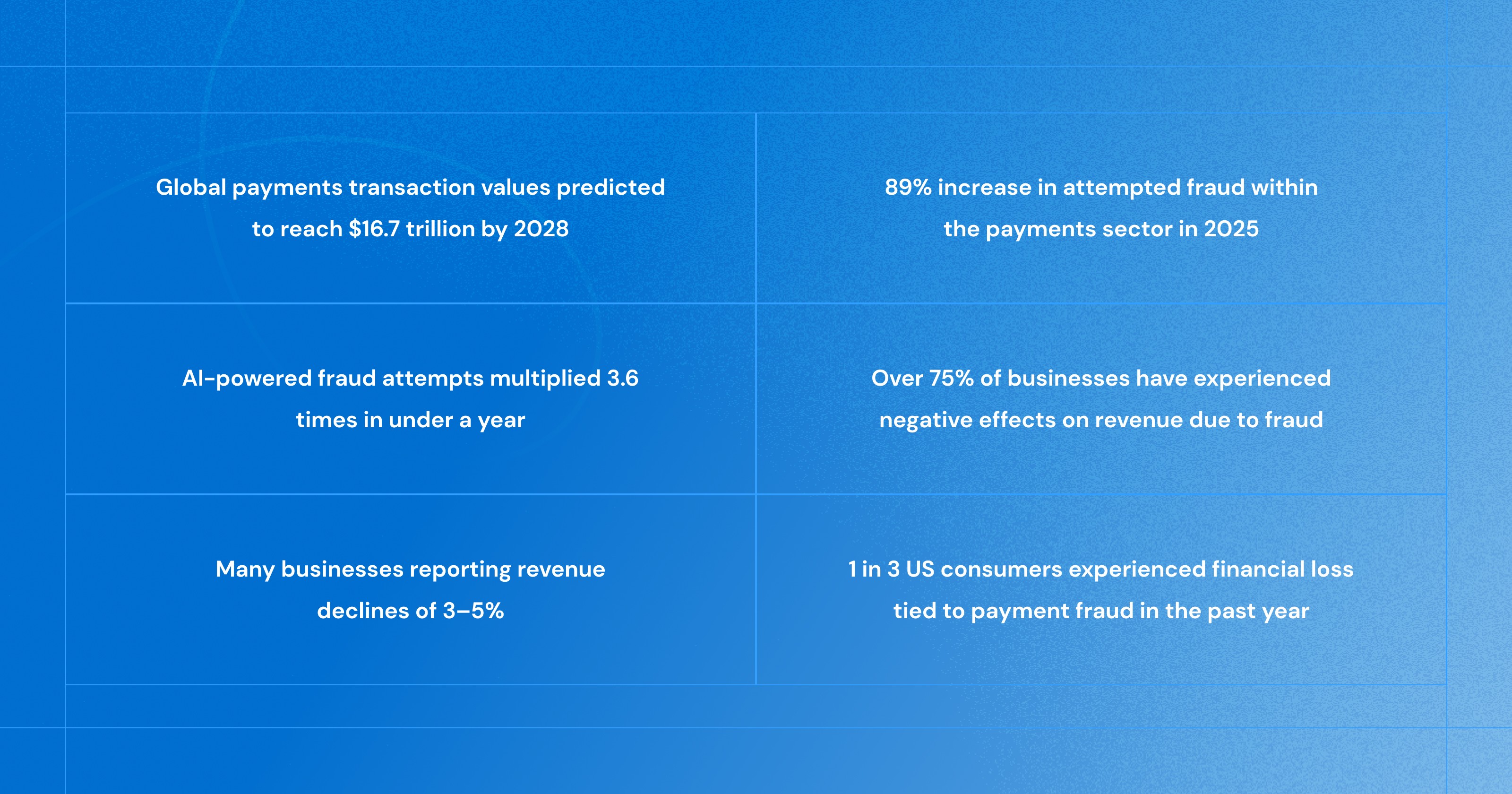

2026 Payment Fraud Trends to Watch

The environment is shifting fast. These are the patterns showing up most clearly heading into 2026.

AI-powered fraud is no longer rare. Fraudsters are using the same machine learning tools that businesses use to defend themselves. Deepfakes, synthetic identities, and AI-generated documents are now common attack vectors not edge cases. Payment fraud trends in 2026 point to a continued arms race between AI-driven attacks and AI-driven defenses.

E-commerce scams are getting more targeted. Random card testing still happens, but more sophisticated attackers are targeting specific merchants with coordinated campaigns. Ecommerce fraud prevention best practices now include real-time behavioral analysis, not just rule-based checks. A rigid rule set written in 2023 probably won't catch what's being attempted in 2026.

Account takeover is up. This one is tied directly to credential stuffing and phishing campaigns. Once an attacker controls a legitimate account, most fraud tools won't flag the transaction because the identity checks pass. Device fingerprinting and behavioral signals are increasingly important here.

Cross-border fraud is harder to catch. As payment infrastructure expands across emerging markets globally - across Africa, Southeast Asia, Latin America, the Middle East - fraud patterns are becoming more regionally specific. A risk rule that works well in one market may generate excessive false positives in another.

The regulatory environment is tightening. Compliance requirements around payment fraud detection are becoming more demanding across more jurisdictions. Meeting them isn't optional, and businesses that haven't automated their fraud monitoring will feel that pressure acutely.

Card Testing Attacks. Fraudsters use automated bots to run small transactions across thousands of stolen card numbers to identify which cards are active before attempting larger purchases. Detecting these attacks requires monitoring transaction velocity and behavioral patterns across many attempts,something fraud orchestration layers are designed to manage.

The Friendly Fraud Problem

Friendly fraud - where a legitimate customer disputes a valid charge - is one of the most under-discussed problems in payments. It accounts for a significant share of chargebacks, and it's genuinely hard to fight because the transaction looks clean from every angle.

The challenge is that most fraud tools are built to catch bad actors from the outside. Friendly fraud comes from customers who passed every check. Addressing it requires a different approach: better transaction documentation, smarter dispute workflows, and data that tells a clear story when you need to challenge a chargeback.

Fraud orchestration helps here too, not by preventing the fraud in the first place, but by generating the evidence trail you need after the fact. Every decision your fraud layer makes is logged. Every rule that fired, every score that came back, every action taken. That data matters when a chargeback hits.

Payment Fraud Orchestration Through MoneyHash

“Modern payment infrastructure should treat fraud signals as part of the transaction flow, not as a separate step. By combining payment orchestration with fraud rules and risk assessment, merchants can make smarter decisions about routing, authentication, and risk handling in real time balancing cost, security, and customer experience. Most fraud tools ask you to trust them. MoneyHash asks you to configure it.” - Ahmed Salem Elzeiny, Lead Solution Architect, MoneyHash.

That's the core difference. Dynamic Fraud, MoneyHash's built-in fraud orchestration feature, is built around the idea that you know your business better than any algorithm does. You define the risk lists. You write the risk rules. You decide when to call a third-party tool and what to do based on its response.

The results speak to this approach. Merchants using our orchestration engine see 1 in 5 fewer fraud cases, a 10% lift in authorization rates, and zero PCI burden - because the system is built to approve more legitimate transactions, not just block more suspicious ones. False positives are expensive too.

Our reach is vast: we operate in more individual markets than most payment stacks have providers in their entire network. That matters because fraud patterns are local. A risk rule tuned for card fraud in Europe looks different from one managing mobile wallet fraud in Sub-Saharan Africa or digital payments in Southeast Asia.

The feature set covers what you actually need for serious fraud management, such as:

Third-party fraud integrations — connect to advanced tools like Forter or Sift through MoneyHash without separate integrations for each.

Risk lists — build lists of customers, IPs, countries, BINs, or any other data point you want to assign a risk level to. Add a new entry and it takes effect immediately.

Risk rules — combine conditions to identify medium and high-risk cases. "Transaction over $500 AND email on blacklist" can become a rule in minutes.

Dynamic 3DS — require 3DS only when risk levels justify it. Low-risk transactions skip it. High-risk ones get the extra layer.

Third-party routing — route flagged transactions to specialized fraud tools automatically, based on the logic you define.

The goal isn't to block more transactions. It's to block the right ones and approve more of the legitimate ones that other systems flag by mistake. That's what a serious fraud management solution looks like in practice.

See It for Yourself

MoneyHash gives you one place to build, manage, and optimize your entire payment operation - from Dynamic Fraud for fraud orchestration, Dynamic Routing for smarter transaction routing, Dynamic Checkout for a localized payment experience, Virtual Wallets for stored value management, and APM integrations that connect you to the payment methods your customers actually use. And that's just the start. Everything works together, in one stack, configured to your business logic.

The best way to understand how it fits your specific payment flows is to see it in action. Book a demo and our team will walk you through the full platform - not a generic overview, but a look at how these products work together for your use cases and markets.

After the demo, you can also get sandbox access to test it yourself. Set up risk rules, build routing flows, and run transactions through the system to see how decisions get made in real time. Book a Demo - then take it for a spin yourself. Visit www.moneyhash.io to get started.

Author:

Ahmed Salem Elzeiny

Lead Solution Architect

With a career spanning fintech, healthcare, telecommunications, and real estate industries, I have developed a strong foundation in software engineering principles, system design, and architecture. My goal is to leverage my technical skills to drive scalable and efficient software solutions.